Table of Contents

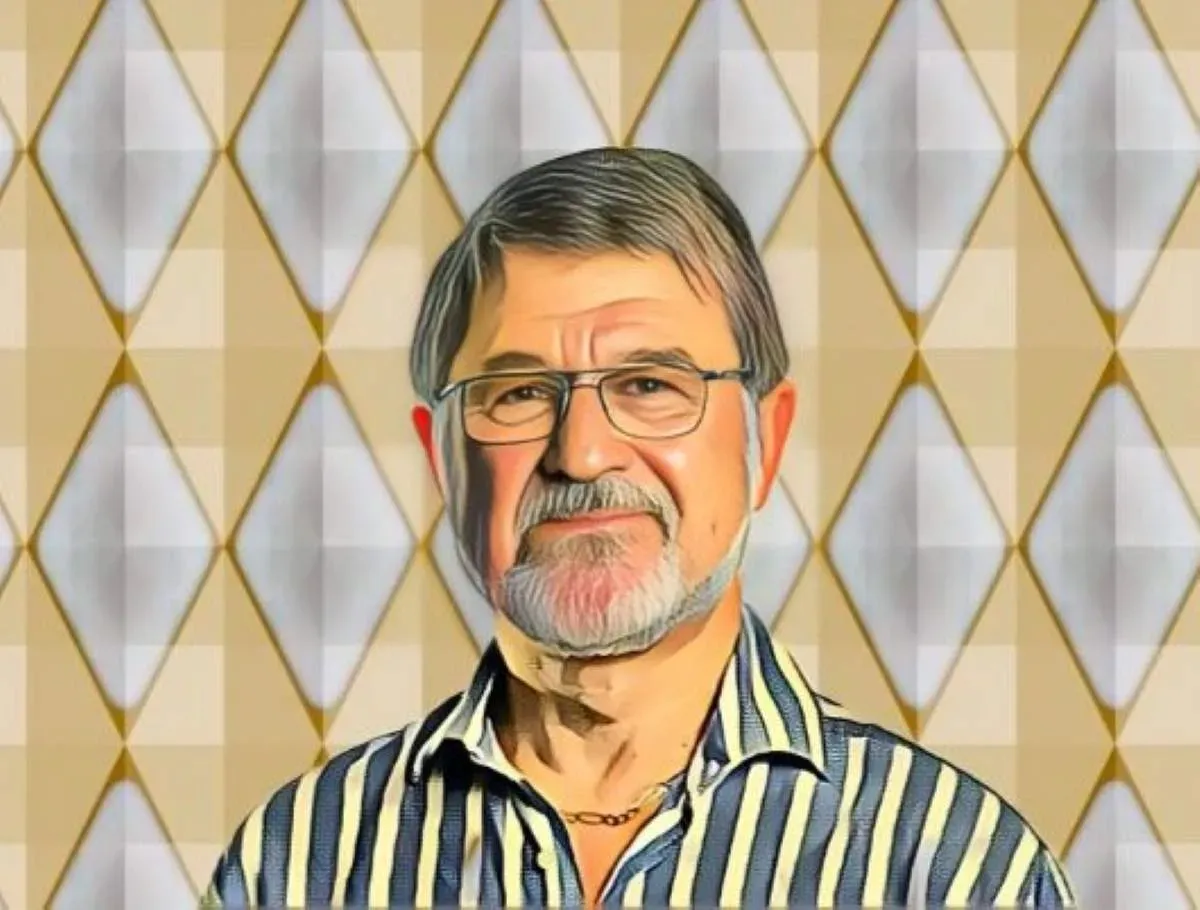

James Mwangi has spent years positioning Equity Group for a breakout into new African markets, and Ethiopia has long been the prize he wanted most. That deal is not moving fast enough. So he is going to Luanda instead.

Equity Group is moving to acquire a majority stake in an undisclosed Angolan bank in 2026, reshuffling its expansion priorities after prolonged regulatory friction in Ethiopia blocked the group's market entry. The pivot is a signal that Mwangi, East Africa's most prominent banker, is not willing to wait indefinitely for one market to open before moving on others.

Ethiopia's banking sector opened to foreign competition for the first time in over 50 years when parliament passed the Banking Business Proclamation in December 2024. But the rules are tight. Foreign strategic investors are capped at a 40% ownership stake in any single domestic lender, total foreign ownership across all foreign shareholders cannot exceed 49%, and minimum paid-up capital is set at five billion birr, to be remitted in foreign currency. Equity has maintained a representative office in Addis Ababa for seven years, positioning itself for entry. It hasn't been enough to close a deal.

While Ethiopia's window stays narrow, Angola's banking sector is opening in a different way. The central bank's new minimum capital requirements are forcing smaller lenders to merge or exit the market, creating a consolidation wave that regional players are moving to exploit. Equity is not alone in seeing the opportunity. Nigeria's Access Bank and South Africa's Standard Bank are among the institutions looking at the same opening.

Angola is Africa's second-largest oil producer, Portuguese-speaking, and increasingly focused on economic diversification after years of oil-revenue dependence. Its banking sector remains underpenetrated relative to the size of its economy, and new capital rules are thinning the field of smaller independent lenders. That combination is attractive.

The Angola pivot comes as Equity sits on the strongest financial base in its history. Mwangi's group posted a 55% jump in profit after tax to KSh75.5 billion, roughly $580 million, for the financial year ended December 2025, its best result since Mwangi joined the bank in 1991 and eventually turned it from an insolvent building society into East and Central Africa's largest lender.

Regional subsidiaries now account for nearly half of the group's banking profitability, validating a decade of aggressive cross-border expansion. The Democratic Republic of Congo, once a bet that skeptics questioned, posted a 58% rise in profit after tax to KSh24.7 billion. Uganda surged 500% from a low base to KSh3.6 billion. Tanzania was up 125%, Rwanda delivered double-digit gains. The Kenyan home unit contributed a 63% increase in profit to KSh39.2 billion.

On the back of those results, the board proposed a dividend of KSh5.75 per share, a 35.3% increase from the prior year and a total payout of KSh21.7 billion. As a 3.39% shareholder in the group, Mwangi is in line to collect more than KSh734 million from that distribution.

"The 2025 performance reflects the success of our deliberate transformation into a diversified, regional financial services group," Mwangi said in a statement accompanying the results. "Our regional subsidiaries now contribute about half of our banking profitability, demonstrating the value of our pan-African footprint and the resilience that comes from diversification."

Mwangi's declared goal is to operate in 15 African countries serving 100 million customers by 2030. The group is currently in seven. Angola would add one more. Ethiopia, when it eventually happens, would add another. The 2030 clock is running, and Mwangi is clearly unwilling to let one market's regulatory pace determine the timeline for the rest.

{kind=link}