Table of Contents

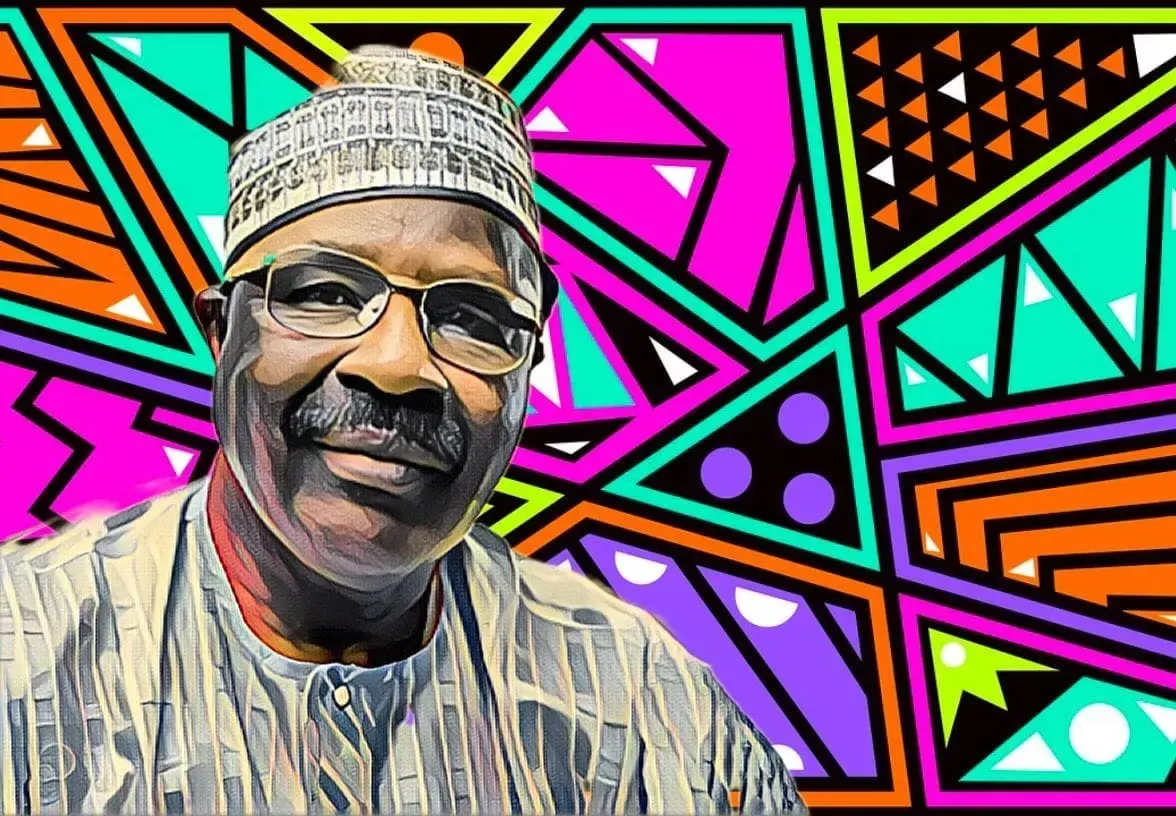

Ahmadou Baba Danpullo, widely regarded as Cameroon's richest businessman, is running into trouble trying to sell his stake in one of the country's most strategically important agribusiness companies, with a weak cotton market and a disappointing harvest making potential buyers cautious about the asset.

Danpullo holds a minority position in Société de Développement du Coton, the state-linked enterprise known as Sodecoton that has served as the backbone of cotton farming across northern Cameroon for decades. According to a report by Africa Intelligence, he had been exploring an exit for months, partly in the wake of moves by former strategic shareholder Geocoton to reduce its own exposure to the company. But the conditions for selling have worsened.

Cameroon's 2025 to 2026 cotton season has been hit by poor output. International cotton prices have softened at the same time. That double blow has cooled the interest of investors who might otherwise have seen Sodecoton as a stable entry point into Central African agricultural supply chains.

Danpullo's holding has previously been estimated at around 11 percent, making him one of the most significant private shareholders in a company where the Cameroonian state remains dominant. At stronger cotton prices, that stake would have carried attractive dividend prospects and strategic appeal. In the current market, the calculation is harder to make.

When commodity prices fall, buyers push for lower entry valuations. Sellers who believe their asset is worth more tend to hold out. That gap between what Danpullo might expect and what prospective buyers are prepared to pay appears to be the central sticking point. The weaker cotton environment has also narrowed the pool of credible bidders.

Price is not the only complication. Any buyer would need to get comfortable with the governance structure of a company that sits at the intersection of private capital and state policy. Sodecoton is not a straightforward commercial acquisition. It supports cotton growers across Cameroon's north, buys their harvests, processes the output and channels production into export markets. In regions where formal employment is scarce, it functions as a major economic pillar. That makes any change in ownership politically sensitive and means prospective buyers carry a heavier layer of due diligence than a comparable industrial transaction might demand.

Danpullo built his fortune across real estate, agriculture, telecommunications and finance, rising from cattle trader to billionaire over several decades. He also assembled one of the largest African-owned commercial property portfolios in South Africa before a legal dispute with lenders drew attention to that side of his business affairs. He is not an unfamiliar figure in complex negotiations.

But Sodecoton is different. Office towers and urban land are easier to value and easier to exit. A cotton company with deep ties to rural livelihoods, farming unions and government policy requires buyers with a longer horizon and a tolerance for operating in a politically watched environment.

The timing of his attempted exit has proved awkward. Cotton markets globally have been under pressure as demand patterns shift, weather risks accumulate and textile consumption trends evolve in ways that affect producing countries unevenly. African producers, including Cameroon, typically feel commodity swings more sharply because margins are thinner and financing costs are higher.

Potential buyers will also be asking a fundamental question: is the current cotton downturn temporary, or does it signal a longer structural shift? If they believe prices will recover, an acquisition at current levels could still make sense. If they are less certain, they may wait for a steeper discount before committing.

That leaves Danpullo with limited options. He can accept a lower valuation now, hold the stake and wait for market conditions to improve, or find a buyer with political alignment and a longer investment horizon who is willing to look past the current cycle.

Any eventual sale will attract scrutiny well beyond the deal itself. Sodecoton's shareholder composition affects the balance between private capital and government influence in a company that Cameroon's policymakers regard as strategic. Farmers and unions would also watch closely.

Danpullo has not announced any final decision. Commodity markets move in cycles, and experienced investors often wait out weak periods rather than take a discounted exit. What is clear is that a stake once considered a prized asset is proving harder to sell than anticipated, and the path to an exit has grown considerably more complicated.

The intelligence satisfies curiosity. The paid briefings satisfy strategy.

Every Monday, Elite subscribers receive an Investor Memo breaking down the deal, the structure and the positioning behind the week's most consequential African wealth story - the kind of analysis that doesn't appear anywhere else.

Twice a month, a Wealth Intelligence brief profiles a single billionaire's holdings, cash flows and expansion pipeline in detail no public source matches.

→ Executive ($25/mo): Daily newsletter + Deep-Dive Reports

→ Elite ($75/mo): Everything above + Investor Memos + Wealth Intelligence + Quarterly Analyst Briefings

Subscribe now

{kind=link}