Table of Contents

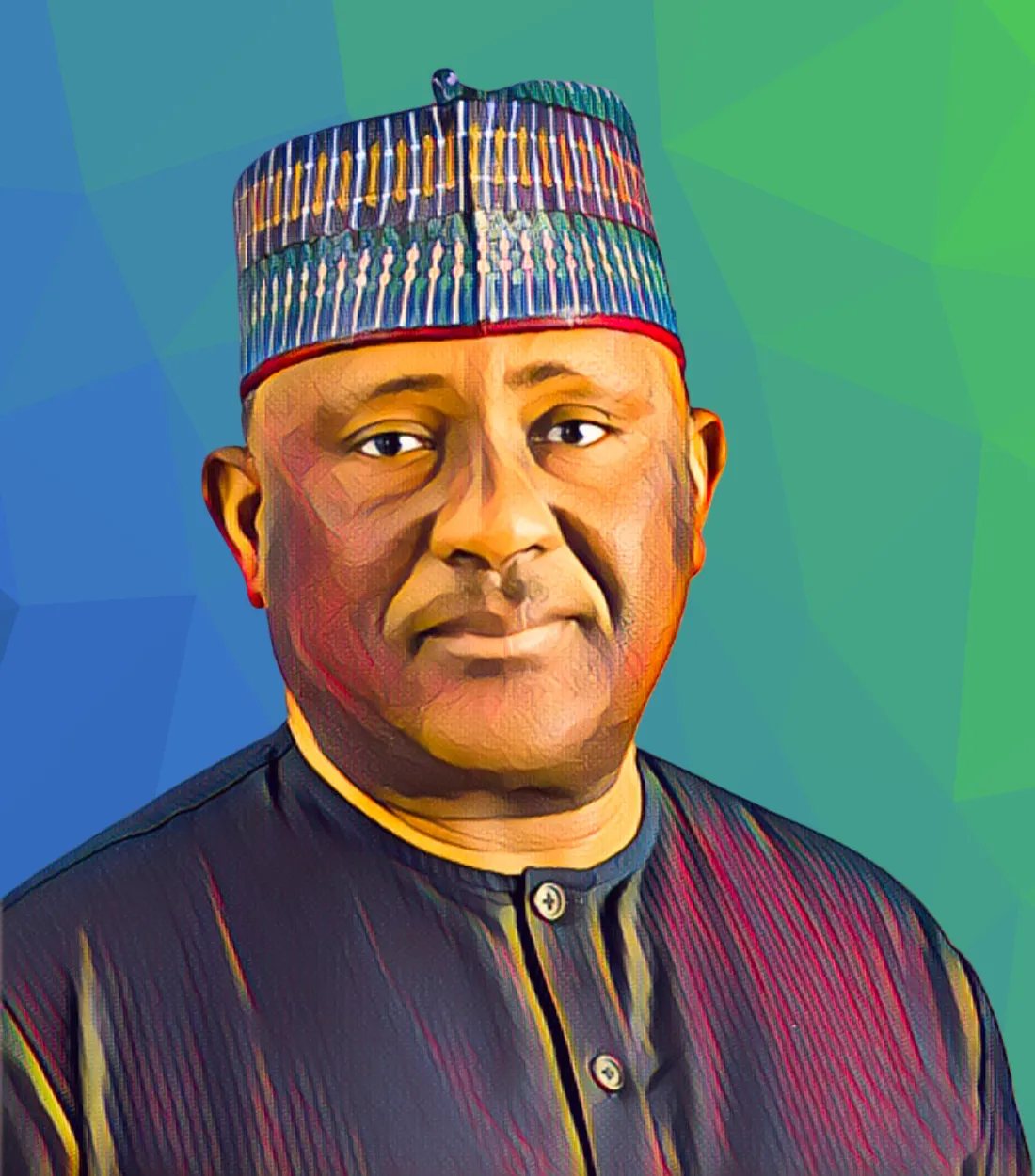

FirstHoldCo Plc opened Friday's session on the Nigerian Exchange on full bid with no offers, with buyers queued and no sellers willing to move, as the parent company of First Bank of Nigeria reported a 72% jump in first-quarter profit that left the market with little debate about where the stock should trade.

By midday, shares had climbed N6.15 to N67.80, a gain of just under 10%, according to Bloomberg data. The move added approximately N49.6 billion in paper value to the stake held by Femi Otedola, FirstHoldCo's billionaire chairman, whose 8.06 billion shares representing 18.12% of the company are now worth roughly N546.5 billion, or about $379.5 million at current exchange rates. That single-session paper gain translates to approximately $34.4 million at the naira's prevailing rate against the dollar.

The numbers driving the session were significant. FirstHoldCo posted a profit before tax of N321.12 billion for the three months ended March 31, up 72.2% from N186.47 billion in the same period of 2025. Profit after tax rose 56.5% to N267.8 billion. Gross earnings climbed 26.8% to N942 billion. Non-interest income more than doubled to N219.2 billion. The result positioned the group as Nigeria's second-most profitable banking institution by absolute profit before tax in the first quarter, behind only Zenith Bank's N360.91 billion and ahead of GTCO at N302.89 billion, Access Holdings at N272.2 billion and UBA at N160.65 billion.

The standout metric was not the profit figure itself but what sat underneath it. FirstHoldCo delivered a post-tax return on equity of 31.6% in the quarter, the highest in the FUGAZ group, the acronym used to describe Nigeria's five largest banks. That ROE figure carried particular weight because the bank is simultaneously completing its recapitalisation, a process that by definition dilutes returns on equity by bringing in fresh capital before it can be fully deployed. Producing a 31.6% ROE in those conditions was not something the market had built into its models.

The result is a direct consequence of a painful strategic decision taken in 2025. Under Otedola's chairmanship, FirstHoldCo absorbed N830 billion in impairment charges to resolve legacy non-performing loans built up over decades, destroying the prior year's profit line in the process. Profit before tax for the full year 2025 fell 70.5% to N235 billion. Analysts at the time described the move as necessary surgery. The Q1 2026 results are the surgery's first clean report. Loan recoveries, the cash the bank is clawing back from assets written off in the cleanup, surged 1,570% to N19 billion in the first quarter from just N1 billion in Q1 2025. The cost-to-income ratio improved from 53.8% at the end of 2025 to 45.2% in the quarter, still behind GTCO's 30.9% but substantially better than Access Holdings at 55.8% and UBA at 61.2%.

The stock's reaction on Friday fits a pattern that has become familiar to investors tracking companies where Otedola holds the chairman's seat. His previous major corporate intervention was at Geregu Power Plc, where he controlled the company before divesting his majority stake in a deal estimated at $750 million in December 2025. During his chairmanship, Geregu's stock became one of the NGX's highest-profile performers. Analysts covering Nigerian equities have begun applying a similar lens to FirstHoldCo, with several noting that the valuation gap between the stock and its peers remains wide enough to close substantially if earnings momentum continues.

The Price-to-Book ratio on FirstHoldCo stood at approximately 0.8 times prior to the rally, meaning investors were paying 80 kobo for every naira of the bank's net assets. GTCO trades at roughly 1.4 times book. Zenith Bank trades at around 1.06 times. Even after Thursday's gain, FirstHoldCo remains below book value, a gap analysts say cannot persist if the bank sustains its current earnings trajectory. Some market participants have described the stock as one of the most asymmetric value trades on the NGX, and Thursday's session added several billion naira of institutional weight to that argument.

A structural catalyst sits on the horizon. Nigeria is scheduled for reclassification into the FTSE Russell Frontier Market Index on September 21, 2026. Reclassification events typically trigger automatic inflows from passive funds that track the relevant index. As a large-capitalisation, highly liquid bank stock with improving fundamentals, FirstHoldCo is a natural recipient of those flows. Analysts expect institutional positioning ahead of that date to provide an additional bid under the shares in the months between now and September.

Otedola became chairman of FirstHoldCo in January 2024, inheriting a balance sheet carrying decades of unresolved bad loans. His 8.06 billion shares, accumulated through a series of open-market purchases and held partly through his investment vehicle Calvados Global Services Limited, represent a bet he has been building steadily and buying into at every available price point since he arrived.

Friday's session suggested the market is starting to agree with his arithmetic.

The intelligence satisfies curiosity. The paid briefings satisfy strategy.

Every Monday, Elite subscribers receive an Investor Memo breaking down the deal, the structure and the positioning behind the week's most consequential African wealth story - the kind of analysis that doesn't appear anywhere else.

Twice a month, a Wealth Intelligence brief profiles a single billionaire's holdings, cash flows and expansion pipeline in detail no public source matches.

→ Executive ($25/mo): Daily newsletter + Deep-Dive Reports

→ Elite ($75/mo): Everything above + Investor Memos + Wealth Intelligence + Quarterly Analyst Briefings

Subscribe now

{kind=link}