Table of Contents

Moroccan billionaire Anas Sefrioui has sold his only cement plant in France, exiting a European asset that had become increasingly difficult to justify on financial and strategic grounds, and turning his attention more fully toward the African markets where his CIMAF cement network is already one of the continent's most geographically spread industrial operations.

Africa Business Plus reported the disposal, describing it as part of a deliberate decision by Sefrioui to prioritise higher-growth opportunities across Africa rather than continue operating an isolated plant in a sector that has become punishingly expensive to run in Europe. The plant was an integrated cement facility in the south of France, held through Sefrioui's cement interests.

The French asset had become hard to justify for reasons that apply across the European cement sector more broadly. Energy costs in France have risen sharply in the post-2022 period. Stricter European Union emissions rules have forced cement producers to invest heavily in carbon reduction technologies, raising operating costs substantially for a manufacturing process that is inherently one of the most carbon-intensive in the industrial world. Slowing construction demand in parts of France compounded the commercial pressure. The combination made it difficult to generate returns that could compete with what CIMAF's African plants are producing in markets where urbanisation and infrastructure investment are running in Sefrioui's direction.

What CIMAF looks like today

Sefrioui launched CIMAF in 2011 through his holding company and expanded it rapidly across West and Central Africa, targeting countries with limited local cement production capacity and rising construction demand. The network now stretches across Ivory Coast, Cameroon, Guinea, Gabon, Burkina Faso, Chad and Congo, among others, making it one of the most geographically diversified cement operations on the continent outside of Dangote Cement's pan-African network.

The regional strategy was built on a simple competitive insight: in a number of Francophone African countries, cement had to be imported at significant cost because no local production existed. Building grinding and integrated production facilities in those markets gave CIMAF a structural cost advantage and first-mover positioning in markets that were growing faster than anywhere in Europe.

That logic has not changed. Africa remains one of the few regions globally where long-term cement demand is expected to rise steadily, driven by rapid urbanisation, population growth and government infrastructure programmes linked to roads, ports, housing and industrial development. The African Continental Free Trade Area has added another layer to that outlook by strengthening expectations of cross-border trade infrastructure investment across the coming decade.

Selling the French plant, whether or not the proceeds flow directly into African capacity, at minimum removes the capital, management attention and regulatory burden of maintaining a sub-scale European asset in a difficult operating environment. The strategic message is clear: Sefrioui is an African industrial investor, not a European one.

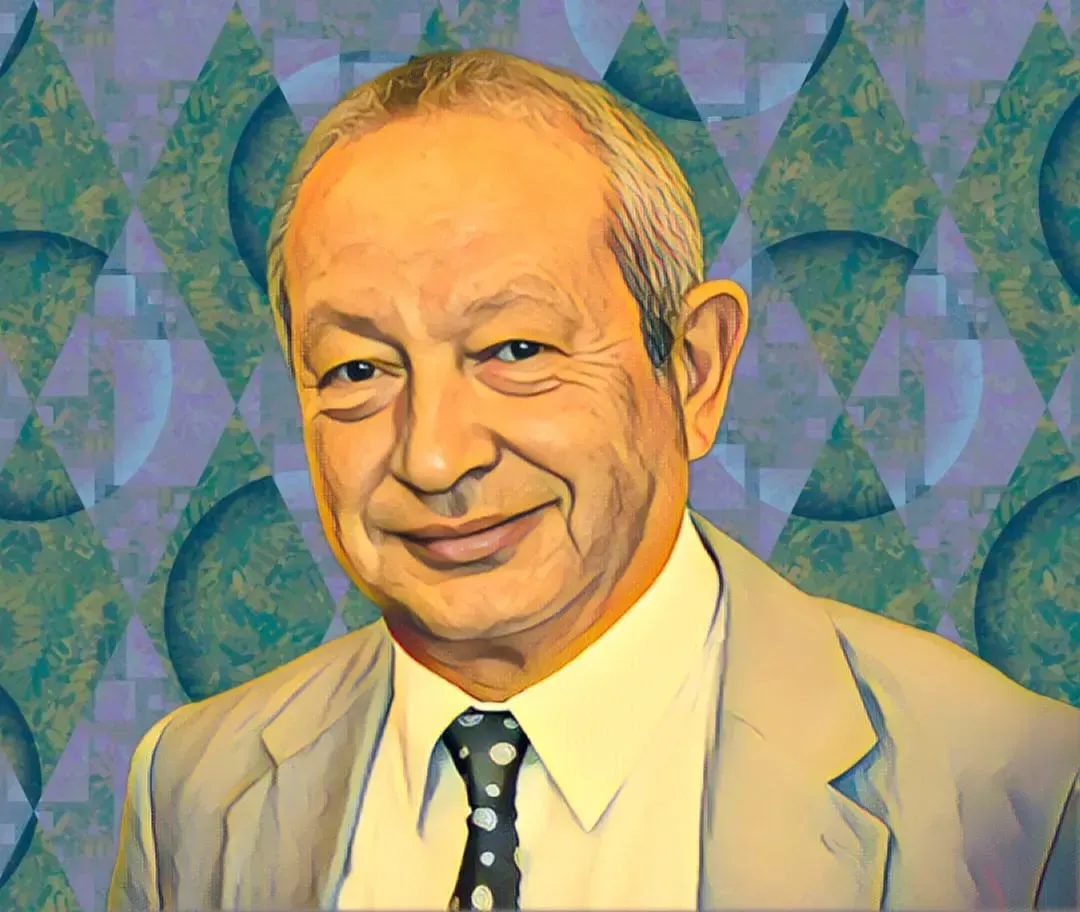

Who Sefrioui is

Anas Sefrioui built his first fortune through affordable housing. Groupe Addoha, the Moroccan real estate developer he founded, became one of the country's largest property companies by partnering with government-backed social housing programmes and building at scale for a Moroccan population that needed homes faster than the private market alone could deliver. The model worked well through much of the 2000s and 2010s, producing a company capable of addressing mass-market demand while generating the profits to fund diversification.

Cement was the natural extension. His real estate operations consumed large quantities of building materials, and the African markets where he saw the same affordable housing dynamic playing out at continental scale needed those materials too. CIMAF became the industrial arm that could supply the raw material for the same urbanisation wave driving his property business, replicated across a dozen African economies.

Forbes estimates his net worth at approximately $1.3 billion in 2026. The valuation has seen some volatility linked to Moroccan real estate share prices over the past year, as the listed components of Groupe Addoha have moved through a period of pressure common to property developers across emerging markets navigating higher interest rates and post-pandemic demand adjustment.

The competitive context

The African cement sector is intensely contested. Aliko Dangote's Dangote Cement remains the dominant continental producer by installed capacity with more than 55 million tonnes annually across 10 African countries. Lafarge, Heidelberg Materials and BUA Cement all maintain significant African operations. Morocco's industrial groups have carved a particular niche in Francophone West and Central Africa, leveraging historical business ties, French-language cultural familiarity and geographic proximity to move more fluidly across borders than some Asian or European competitors.

Sefrioui has benefited from that Moroccan positioning. CIMAF's expansion has been part of a broader Moroccan commercial push across the region over the past decade, alongside Moroccan banks, insurers and telecoms operators that have all deepened African footprints as Rabat's diplomatic and economic ties with sub-Saharan African governments strengthened.

The question now, as Africa Business Plus noted, is whether the capital released from the French sale accelerates CIMAF's expansion into additional African markets, deepens capacity in existing ones, or serves some combination of both. The competitive pressure is intensifying as more players recognise what Sefrioui identified more than a decade ago: that Africa's cement demand story is long-duration and structural, not cyclical.

The intelligence satisfies curiosity. The paid briefings satisfy strategy.

Every Monday, Elite subscribers receive an Investor Memo breaking down the deal, the structure and the positioning behind the week's most consequential African wealth story - the kind of analysis that doesn't appear anywhere else.

Twice a month, a Wealth Intelligence brief profiles a single billionaire's holdings, cash flows and expansion pipeline in detail no public source matches.

→ Executive ($25/mo): Daily newsletter + Deep-Dive Reports

→ Elite ($75/mo): Everything above + Investor Memos + Wealth Intelligence + Quarterly Analyst Briefings

Subscribe now

{kind=link}