Table of Contents

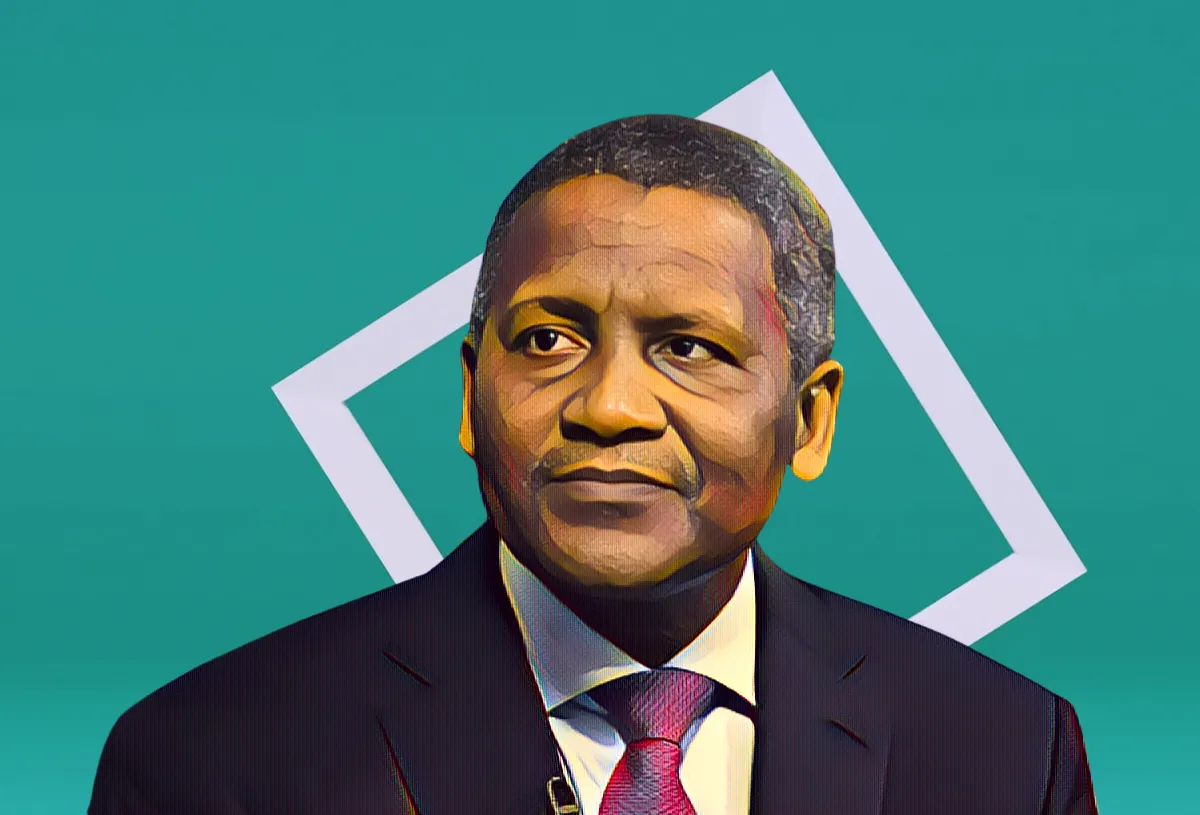

Abdul Samad Rabiu has a simple test for whether African economic sovereignty is real or rhetorical: try selling sugar in Mali.

The BUA Group chairman recently walked into that market and ran straight into a wall. Not because Mali had a domestic sugar producer worth protecting. It did not. The obstacle was a Malian importer with government connections who did not want the competition. Duties and VAT were applied in ways that made Rabiu's sugar uncompetitive on price, even though it would have cost Malian consumers less than what they were already paying.

"I wouldn't have argued if it were a situation where a local producer is being protected," Rabiu told The Africa Report in an interview published Wednesday. "That was not the case." He said he even offered to build a refinery in Mali. The government preferred to keep importing.

Rabiu, who chairs BUA Group, the Nigerian conglomerate whose cement and food businesses generated a combined revenue of roughly $2.6 billion in 2025, was speaking from his offices in London's Mayfair. The conversation ranged across freight costs, forex reform, cement capacity and the African Continental Free Trade Area, but it kept returning to the same point: the gap between what African governments say about industrialisation and what they actually do when it costs someone in power something.

On the AfCFTA specifically, he is not impressed. "It's not working," he said, at least not in the ways that matter for a company trying to sell processed goods across borders. Regional integration on paper, he argues, is meaningless if governments use tax and duty policy to shield connected importers from African competitors.

The Mali frustration sits alongside a broader investment decision that Rabiu described with visible impatience. In February, BUA Group signed a memorandum of understanding with Abu Dhabi's AD Ports Group and MAIR Group to explore sugar refining, edible oils and logistics projects in the United Arab Emirates. The attractions were practical: functioning ports, available energy, reliable infrastructure and policy that does not require a CEO to improvise his own supply chain. "It's sad for Africa," Rabiu said. "We cannot even embrace some of our people to come and help us develop the continent."

That comment carries real weight coming from the man who built BUA Cement into a 17 million tonne per year operation and is now pushing it toward 20 million tonnes with a $240 million expansion agreement signed with China's CBMI in January. BUA Cement's Sokoto factory sits on limestone, gypsum and gas that are all local. The economic case for making cement there is not political. It is geological. Rabiu's argument is that protection worked in Nigerian cement because there was something real to protect.

"Obasanjo did that because he wanted local companies to produce cement locally," he said of former President Olusegun Obasanjo's import restrictions. "Today, Nigeria is an exporter of cement."

But he is clear that the cement story is not transferable to every sector through tariffs alone. What governments need to do first, he argues, is lower the cost of operating on the continent. Energy, roads, ports, macroeconomic stability. Without those, domestic companies spend more time surviving distortions than building scale.

He described the years under former Nigerian President Muhammadu Buhari as a particularly vivid example of a system that rewarded access over efficiency. "I was spending more time chasing forex than selling my food products," he said. He flew to Abuja every two weeks to see the central bank governor. "You needed to do that to survive."

The reforms under President Bola Tinubu have been painful, he acknowledged, and households are still squeezed. But the old system of rationed dollar access was producing something worse than pain. It was producing strategic distortion. Companies were managing their forex position rather than their business. BUA, he said, has largely cleared the forex losses that accumulated under that regime. BUA Foods reported profit after tax of N507.7 billion in 2025, BUA Cement N356 billion.

On the food side, he is candid about the exposure that remains. BUA imports most of its food raw materials, and freight costs from India have surged. His answer is backward integration: a sugar project in Nigeria using Israeli drip irrigation technology that he says will eventually produce 300,000 tonnes of sugar annually and create more than 20,000 direct jobs. "These things take time, especially agriculture," he said. "Once you get them done, they are forever, they are for generations."

BUA is also building a 700-tonne-a-day mini-LNG project to move gas from Kogi to Sokoto, cutting energy costs for its cement expansion without waiting for the state to solve the problem. It is the same logic as the generator in the backyard, scaled to an industrial operation.

Rabiu's position is not a call for closed economies or blanket protection. It is something harder to argue against: build the real conditions for industry first, make regional markets function in practice rather than on paper, and stop protecting the people who are blocking African capital from doing what it is trying to do.

The intelligence satisfies curiosity. The paid briefings satisfy strategy.

Every Monday, Elite subscribers receive an Investor Memo breaking down the deal, the structure and the positioning behind the week's most consequential African wealth story - the kind of analysis that doesn't appear anywhere else.

Twice a month, a Wealth Intelligence brief profiles a single billionaire's holdings, cash flows and expansion pipeline in detail no public source matches.

→ Executive ($25/mo): Daily newsletter + Deep-Dive Reports

→ Elite ($75/mo): Everything above + Investor Memos + Wealth Intelligence + Quarterly Analyst Briefings

Subscribe now

{kind=link}